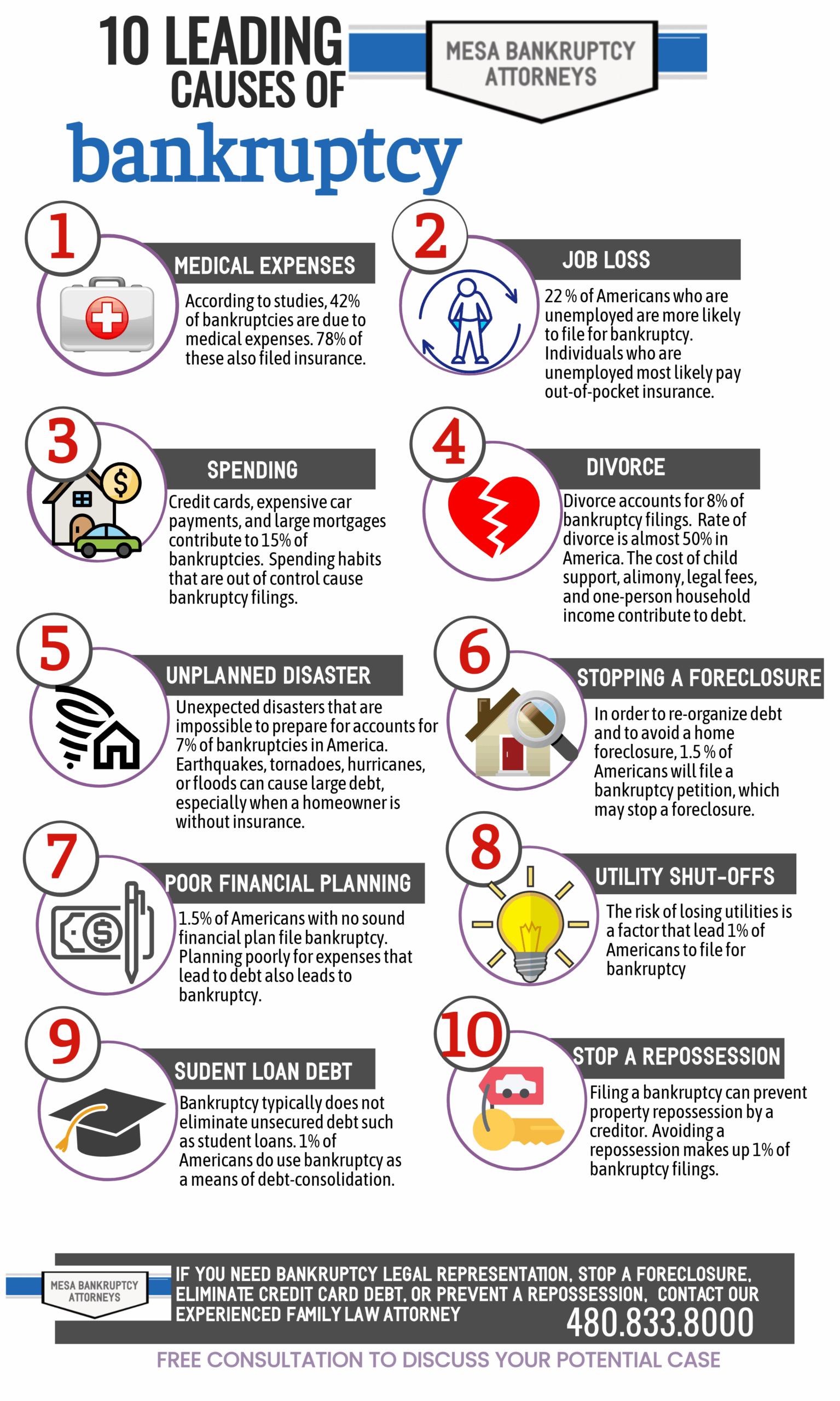

Bankruptcy is an option for many Mesa, Arizona residents with debt. Whatever the reason it accumulated, overwhelming debt affects an individual’s personal, professional, financial, and family life. The attorneys at Mesa Bankruptcy Lawyers Law firm are dedicated to exceptional legal representation and helping Arizona residents eliminate or reduce debt. Is bankruptcy the right means to eliminate your specific debt / financial situation? Both Chapter 7 and Chapter 13 bankruptcies are viable options to many debt-related financial issues. Consult with an attorney to find out which filing is best for your unique debt case, and to get information on your rights as a debtor as well as debt-relief options.

Sometimes debt is caused by an unplanned disaster, unforeseen medical expenses, or loss of a job. Other times debt happens because of poor financial planning or overspending. Despite best efforts to make monthly payments and stay ahead of debt, it sometimes becomes too overwhelming. Bankruptcy is an option when you need to take control of debt, and achieve a financial fresh start. Because of an automatic stay, when a bankruptcy petition is filed, it puts a stop to wage garnishments, repossessions, or a foreclosure.

For years, Chuck E. Cheese has been a favorite for children, especially for birthday parties. The chain features pizza and other kid-friendly fare, along with video games, prizes, and play equipment. Unfortunately, like many restaurants and other businesses, COVID-19 has decimated profits for the past few months and for the unforeseeable future. The Kid’s Birthday Party/Restaurant may have to file for bankruptcy protection.

Company Information

Chuck E. Cheese was founded in 1977 in California, but currently runs out of Texas. There are 615 Chuck E. Cheese locations worldwide, with 610 of those being in 47 of the United States. The chain is owned by the brand CEC Entertainment.

Struggles Due to the Coronavirus Pandemic

Although many restaurants have been able to continue serving takeout and delivery, Chuck E. Cheese quickly realized its clientele patronized them for their atmosphere and activities, not the pizza itself. Public video games and play equipment aren’t acceptable during the pandemic, as it would prevent an easy opportunity for the virus to spread. The chain reports that profits are down 21.9% from this time last year, and it has had to lay off 17,000 employees since March. The company also included that it was considering bankruptcy in this report. Despite all of these problems the chain announced it would be giving bonuses to three top executives to guarantee they stay with the company. If Chuck E. Cheese files bankruptcy due to the coronavirus pandemic, it will be joining the likes of big names like JC Penney, Neiman Marcus, and Pier 1 Imports.

In an effort to recoup some losses and avoid laying off and furloughing all of its employees, the company took a unique approach to sales during the pandemic. Eagle-eyed pizza eaters on delivery services noticed that a chain called “Pasqually’s Pizza and Wings” had the same exact addresses as Chuck E. Cheese. The chain created a pseudonym based on one of mascot’s band members to sell to those too embarrassed to be seen eating Chuck E. Cheese pizza.

Chuck E. Cheese and Chapter 11 Bankruptcy

If the chain files bankruptcy, it will more than likely utilize Chapter 11. Chapter 11 can be used by individuals and by businesses, usually those with significant assets and debts that will be particularly complicated to reorganize. Chuck E. Cheese specified that it would be a Chapter 11 filing if the company does end up filing bankruptcy.

In Chapter 11, the filer’s top creditors will form a panel to assist in reorganizing the bankruptcy debts. Along with the bankruptcy trustee assigned to the case, the panel will make sure that the reorganization is fair for the company and all of its creditors. The company can remain operating and maintain basic management decisions, big business decisions have to be approved by the panel. Alternative debt repayment methods, like ownership and stock options, may be available in a Chapter 11.

When filing bankruptcy, most companies choose between Chapter 11 and Chapter 7 bankruptcy. Chapter 7 liquidates unsecured non-priority debts. It also provides the option to surrender financed assets that are no longer a good investment. Only the trustee will oversee the case, and creditors can appear at the 341 Meeting of Creditors but not form a panel for the case. The drawback is that the company will be forced to cease operations. All of the company’s remaining assets must be surrendered and will be sold to be distributed amongst the company’s creditors.

Personal Bankruptcy Chapter 13 and Chapter 7

Personal bankruptcy filers also have the option to file Chapter 7 bankruptcy, along with Chapter 13. Filers will have their financial slate cleared of debts like credit cards and medical bills, but the benefits are not available to everyone. Assets must have not more equity in them than each state’s applicable exemption value. The filer must either make less than the state’s median monthly income for their number of family members, or prove their disposable monthly income is low enough through the Means Test. There are also waiting periods in between filing most chapters of bankruptcy. Those who don’t qualify for Chapter 7 will usually qualify for Chapter 13 bankruptcy.

Chapter 13 bankruptcy reorganizes debts into a payment plan that lasts 3-5 years, depending on the filer’s income relative to the state median. Some debts, like the balance on a car loan, or arrearages on child support, will be paid in full in the plan. Some unsecured debts may only receive a portion of the debt they are owed. Filers must prove they have enough income to feasibly make minimum monthly payments. There are also limits on how much debt they can have: $419,275 in unsecured debt and $1,257,850 in secured debts.

The spread of coronavirus has impacted businesses and individuals alike. If you are struggling, you should consider how bankruptcy may be able to help you. Our Mesa Bankruptcy Office offers free consultations to help you do just that. Call today to schedule a free consultation to speak to one of our experienced bankruptcy attorneys. We offer free consultations either in office or by phone. We look forward to assisting you.

Bankruptcy is a very helpful solution for challenging financial problems. For instance, several individuals have a big charge card debts that become very tough to be worthwhile. These individuals may simply have to create a fresh break with a painful fiscal past and start things over fresh.

Chapter seven bankruptcy, likewise referred to as a “straight bankruptcy” or a “liquidation bankruptcy”, allows qualifying individuals to discharge the debts of theirs. With Chapter seven bankruptcy, you might be ready to eliminate your most important debts. These debts are able to include: medical bills, certain loans, credit cards, and court judgments. Basically, all unsecured debts are discharged in a Chapter 7 Bankruptcy.

Nevertheless, in case you are one of the numerous individuals considering bankruptcy in Arizona, you must know that there are particular debts chapter seven will not eliminate. Below are some of those debts. This is not all of the things that are not able to be discharged by declaring bankruptcy.

The following are 4 kinds of debt that Chapter Seven Bankruptcy will not discharge:

Spousal Maintenance or Alimony: If you are filing for bankruptcy after you have actually been divorced, you will have to continue making pre established payments to your ex spouse.

Child Support: Similar to alimony, you should continue paying some kid support.

Student Loans: Lots of people seek out bankruptcy since the student loans of theirs are too high. Unfortunately, chapter seven bankruptcy won’t eliminate any debt you built up as an outcome of pupil loans.

Penalties and Fines: When you broke the law, you still need to spend some court imposed financial penalties. This consists of fines from infractions, felonies, misdemeanors, and much more.

This article shouldn’t be considered as legal advice. When you are contemplating bankruptcy or maybe another form of debt relief, you have to talk to an Arizona bankruptcy legal professional for guidance. If you are in Pinal, Pima, or Maricopa County in Arizona and also seeking legal assistance, our Arizona debt relief staff is happy to assist.

Mesa Bankruptcy Lawyers is focused on assisting families find help out of the concern of debt along with other financial problems. With thousands of successful Arizona bankruptcies filed, our AZ bankruptcy lawyers have furnished good direction on all debt help to customers throughout Arizona.

An Influx of Business Bankruptcies in Arizona is on the Horizon

For most of 2020 so far, coronavirus has spread like wildfire. What originally was only a blip on the United States’ radar resulted in most states enacting quarantine and stay-at-home orders to slow the spread of the virus and “flatten the curve.” While stay-at-home orders are starting to expire or be loosened, business won’t be returning to normal any time soon. The coronavirus pandemic has caused production and supply chain issues. Some venues that do reopen will be forced to operate at limited capacity that will increase gradually as quarantine measures loosen. For example, gyms and restaurants will have to remove equipment and tables to maintain a 6 feet distance. Companies will also have to consider clients’ reluctance to come in immediately after quarantine is lifted, and employees’ similar reluctance and scheduling issues due to lack of childcare.

Although many businesses are receiving government relief, it won’t be enough to save some. If the economy doesn’t pick back up soon, businesses will have to consider bankruptcy as a method of dealing with mounting debts.

Business owners consider bankruptcy will have to decide between two chapters: Chapter 7 and Chapter 11. Chapter 7 is typically utilized by smaller businesses that intend to close and remain closed. It is especially useful for businesses where the company owner is personally liable for business debts. A Chapter 7 bankruptcy discharges most unsecured nonpriority debts. This means that the business owner will also be able to discharge personal debts, such as credit cards and medical bills, in the bankruptcy. There are income and asset value limits to file a Chapter 7 bankruptcy, but small business owners will likely qualify if their business is operating in the negative.

For larger businesses and those that wish to remain operating, Chapter 11 may be available to them. A Chapter 11 bankruptcy reorganizes a business’s debts so that paying them off is more feasible. In a Chapter 11 bankruptcy, the business owner will remain in control of day-to-day operations but larger decisions will have to be approved by the court. If you are a small business owner whose interest is piqued by a Chapter 11, proceed with caution.

The court filing fee for a Chapter 11 bankruptcy is $1,717 compared to only $335 in a Chapter 7. While it is almost always preferable to file with an attorney, it isn’t inconceivable to successfully discharge a Chapter 7 bankruptcy pro se, or without an attorney. Filing Chapter 11 without an attorney is nearly impossible, and the attorney’s fees will be much higher than in a Chapter 7. Unlike a Chapter 13 bankruptcy, which lasts 3-5 years, there is no set time frame for a Chapter 11 bankruptcy. A Chapter 7 bankruptcy typically lasts 3-5 months.

If you own a business that is struggling due to the pandemic, you don’t need to wait for quarantine orders to be lifted to get help. Our office is available for phone consultations that are free of charge. Our experienced attorneys can discuss your options, guide you through the bankruptcy process, and offer affordable payment plan options. Call today!

Coronavirus Pandemic May Force AMC Theaters to File Bankruptcy

Mesa Bankruptcy Lawyers and Staff on 4/13/2020 write:

Life is changing rapidly for people and businesses across the country as the spread of coronavirus has forced government officials to issue stay-at-home orders. Gatherings of 10 or more are banned almost everywhere, causing businesses that naturally create gatherings- such as movie theaters- to close. AMC theaters nationwide, including all of the AMC theaters in Mesa and throughout Arizona are at the mercy COVID-19. This is possibly making AMC Theaters to file bankruptcy.

AMC Mesa Grand 14, 1645 S Stapley Drive, Mesa, AZ 85204

AMC has 634 locations in the US and Canada and more than 1,000 worldwide. There are currently 12 AMC theaters in Arizona. Like many businesses, AMC was forced to close March 16, 2020. More than 600 of AMC’s corporate employees, including the CEO, have been furloughed. It is estimated that AMC is currently running at a $155 million loss per month. The company likely only has enough liquidity to last until June or July. AMC already had $4.9 billion in debt before Coronavirus pandemic started.

Massive debts that will continue to grow combined with AMC’s decision to stop paying its landlords starting in April mean that the closure of your Local AMC Theater (AMC Mesa Grand) may be permanent. Since many Americans are experiencing reduced income, even when movie theaters can reopen, they won’t have the budget for discretionary entertainment purchases such as movie tickets. Those who do have money to go to the movies when the pandemic has passed will probably spend their money elsewhere since they’ve spent the last few months indoors watching movies.

AMC Theaters is not Alone with Financial Woes

AMC Theaters is not the only entertainment company facing financial woes due to the coronavirus pandemic. Disneyland and Broadway are shut down, along with Arizona’s busiest movie theater chain, Harkins Theaters. Actually, every movie theater in Arizona is closed for showing films. A few of the “Dine In Theaters” in Arizona are still serving food to go, with mixed success.

Additionally, the first name in acrobatic entertainment, Cirque du Soleil, is also on the brink of bankruptcy. Major studios are delaying the release of big-budget films, like Pixar’s Soul and Disney’s Mulan. Sony has delayed the release of all of its summer films until late 2020/early 2021. This means the movie production industry will be slowing down. If you know anyone who works on movies, you know these are the type of people who insist on seeing every movie in theaters and refuse to sneak in snacks.

During the recession of 2008, the U.S. saw a 33% increase in bankruptcy filings. It is reasonable to expect a similar increase in bankruptcy filings due to the spread of coronavirus. Businesses aren’t immune to this, and those that don’t receive forms of government bailout will be particularly susceptible. Only time will tell which businesses will survive the pandemic, but bankruptcy isn’t a death sentence. Kodak, Jack in the Box, and Best Buy are examples of businesses who successfully recovered after a bankruptcy.

This is one of the questions that our Arizona bankruptcy lawyers often are asked. Many people who need to declare bankruptcy have a favorite credit card that they want to keep even after they have filed for bankruptcy protection.

Unfortunately, you can not pick and choose which debts you are wanting to include in your bankruptcy. Thus, in a word “No” you can not keep one of your cards when filing for bankruptcy in Arizona. We understand that it makes no sense, if you want to pay back some of your debt, it just isn’t fair to your other creditors. An example of how this might work is: You have a balance that you want to Discharge on your Mastercard but want to continue to pay the personal loan that you borrowed from your work’s credit union. That is not something that you can do. Picking and choosing debts to include in bankruptcy is not allowed. Credit Cards with Zero Balance in Bankruptcy

Often, people will tell our experienced bankruptcy attorneys that they chose not to include a creditor on their bankruptcy because the card had a zero balance. Just because they don’t owe money on a card does not make it a card that they can choose not to include. In fairness, usually they are wanting to hang on to that credit card because it is $0 balance and they hope it will help them re-establish their credit after filing bankruptcy. Unfortunately, the lenders (issuers of the credit card) don’t look at this the same way. Most often, the lenders subscribe to services that follow and update current bankruptcies that are filed. Thus, the lenders compare bankruptcy filings to their own database. Any active account that the lender might have (Even with a $0 Balance) that matches up to a bankruptcy case will lose borrowing privileges. Your credit card will be canceled, even sans a balance. Can I Exclude a Credit Card when Declaring Bankruptcy? It’s an Important Card. So, what if I just exclude a card and don’t tell anyone about it? Will that allow me to keep a credit card when declaring bankruptcy? Once again, no matter how important the credit or department store card might be, excluding the account and/or the card is simply not an option. We feel that you should use one of the federal debt relief programs: Chapter 7 or Chapter 13 in order to start a new debt freeChapter of your life.

Coronavirus Affects Bankruptcy Courts Closures for Near Future

Panic over the spread of Coronavirus has increased drastically in the past few weeks. The Coronavirus has caused major events and organizations to suspend activities, cruise ship passengers are being quarantined, even toilet paper is out of stock at stores due to citizens stockpiling specific items.

Even the bankruptcy industry is seeing the effects of this pandemic. Arizona 341 Meetings of Creditors held at Bankruptcy Courts that have been scheduled until March 31, 2020 have been postponed. Anyone who has recently filed bankruptcy, or is considering filing soon needs to understand how this will affect a bankruptcy case.

If you have already filed for bankruptcy:

If your bankruptcy case has already been filed and you have a Meeting of the Creditors on the schedule on or before March 31, 2020, that 341 Hearing will be temporarily postponed. While waiting to hear about your new court date, please be patient. Your lawyer likely will not have any information about the new court date. However, as soon as the attorney receives notice of the new court date, he/she should inform you about the new scheduled date and time. Understand that once your bankruptcy petition was filed, an automatic stay of protection did go into effect, preventing any creditor from collecting on your debts. The automatic stay holds until your case is discharged, which is typically around 60 days after the Meeting of Creditors. Therefore, if your 341 Hearing is postponed, the stay will remain in place and protect you until your bankruptcy case is discharged. Having your 341 Hearing postponed also means that the amount of time before you can get an FHA loan will also be delayed.

If you are considering filing bankruptcy:

Our law firm files bankruptcies electronically, so the Bankruptcy Court’s closing will not affect your ability to file. The 341 Hearing, however, may be scheduled out further than the typical 30-45 days. If you are making any travel plans in the next couple of months, keep this in mind. Because the bankruptcy will be filed with the court, you will still have the automatic stay of protection to stop creditors from collecting debt until the entire bankruptcy is discharged.

If you have any concerns about how the Coronavirus may affect your specific bankruptcy case, please contact our law firm. The present Coronavirus epidemic is becoming a factor in many life situations. Consult with an experienced Arizona bankruptcy lawyer with any questions you may have regarding and existing or potential bankruptcy.

A serious concern of many Americans is their medical financial situation. It is difficult to pay off extensive medical debt and other costs that are incurred while receiving medical care. Mesa Bankruptcy Lawyers can provide you with experienced legal representation, information, and assistance if you need guidance as you work through medical debt.

Medical debt can be wiped out through bankruptcy, but will your Doctor eliminate you as a patient?

The U.S. spent around $3.5 trillion on health expenses, more than any other country in the world. Some experts predict that the average healthcare cost per person in the U.S. will be about $15,000 by 2023. Many individuals are dealing with overwhelming medical bills. In fact, approximately 25% of bankruptcy cases include significant medical debt.

Will your medical provider drop you after you file for bankruptcy?

A legitimate and common concern is not knowing if a person will lose their doctor if they file bankruptcy to discharge medical debt owed.

Doctor bills are unsecured debt, and can be eliminated in a Chapter 7 bankruptcy. If you file bankruptcy and owe money to your doctor, this debt would be listed in your bankruptcy petition. This doesn’t necessarily mean that you have to change physicians.

The short answer is, in an emergency medical situation, regardless of the ability to pay or insurance status, everyone is entitled to initial treatment. A federal law called the Emergency Medical Treatment and Labor Act ensures that anyone who seeks medical attention in an emergency department be stabilized and treated.

When dealing with a non-emergency health provider (including primary physician) may refuse treatment if their fees have been discharged in a bankruptcy. Most medical providers, however, do understand why clients need bankruptcy protection when faced with overwhelming medical debt. Many physicians continue to keep patients as long as they show willingness to pay for future visits. Also, if a medical bill cannot be paid on time, it is crucial that your hospital or doctor’s office be notified immediately. Also, the facility should be able to give you insight on what would happen to your patient status if you do file bankruptcy.

The signs are posted in the stores already as Gymboree, the San-Francisco based major children’s clothing retail store, is reportedly filing Chapter 11 bankruptcy. Additionally, the retail giant will close all 800 of it’s stores including those in Phoenix, Tucson, Mesa, and throughout the valley.

With over one billion dollars of debt, Gymboree is expected to not only file for bankruptcy in the past 2 years, but this 2nd bankruptcy protection, but this 2019 bankruptcy should force Gymboree to close all of it’s stores.

Gymboree has filed for bankruptcy protection before. In 2017, Gymboree filed for bankruptcy protection which led to the closing of 350 stores. Now the company has around 900 retail stores in the U.S. and Canada operating under the three brands. The 2017 bankruptcy filing allowed the company to re-organize it’s debt. The hope was that this debt reorganization would allow the company to make a comeback and not only survive but thrive. It appears the first bankruptcy is going to end up as a failure.

Mesa Gymboree to Close as Company Files for Bankruptcy

The children’s clothing retailer filed for bankruptcy for the second time in less than two years earlier this week. This bankruptcy will bring about the end of its flagship brand. Many stores, once staples in malls and strip malls alike, are facing a similar fate. The on-line presence of Amazon, Walmart Delivery, and even Ebay have forced brick and mortar stores out of business.

Gymboree Group after filing bankruptcy, said it plans to start closing all of its Gymboree and Crazy 8 branded stores, according to the filing. Thus, about 800 stores will soon close.

A report from The Wall Street Journal states that the company will file bankruptcy in order to liquidate Gymboree, Crazy 8, and Janie and Jack stores. The Janie and Jack stores may be saved if a buyer is found by the company for the brand. Currently, approximately 139 Janie and Jack stores are in operation across the nation.

Initially, Gymboree was founded in the 1970’s. Initially, the company offered activity and music classes. Later, in the 1980’s they launched a chain of clothing stores. The clothing stores are what they are most noted. In 2016, the Gymboree Play & Music became a standalone brand owned by an education company. The bankruptcy filed earlier this week, according to representatives, does not include these franchised Play & Music centers.

Thus, with many of our favorite stores and retailers going out of business and filing bankruptcy, it becomes obvious that financial hardship can hit even some of the most established brands. Life for individuals can throw us tough times that may lead to bankruptcy or other tough financial times. Debt relief and a fresh start is only a call away. Contact an Arizona debt relief lawyer and find out the many options available to you.

Wage Garnishments: Can you get back the money that was garnished from my check after filing bankruptcy in Arizona?

Declaring bankruptcy stops wage garnishments from creditors where they are in the process. However, you won’t necessarily get any of the money back that has already been taken from you through the garnishment. The idea is to stop a garnishment before your creditors take action against you. That is the best way to assure that you won’t lose any of your hard-earned money in a garnishment.

A bankruptcy filing will stop any future pay checks from being garnished. Any funds that had been taken prior to the filing of your bankruptcy petition will not be returned. Your bankruptcy trustee may be able to recoup any funds taken up to 90 days prior to your filing. However, those funds are considered those a preferential payment to a particular creditor. The bankruptcy trustee takes that money and uses it in your bankruptcy estate to be distributed evenly among all of your creditors.

However, sometimes a garnishment will continue to be taken after the filing of your bankruptcy petition if proper notification is not given and those funds are able to be returned. Seeking the assistance of our Mesa bankruptcy attorneys is the best way to assure that your wages aren’t garnished any further.

File Your Bankruptcy Prior to Your Payroll Cutoff

It is important to realize that your filing date must be before the end of your pay period, not your pay date. If your pay period ends before the date of your bankruptcy filing those funds will also be lost. Time is of the essence when contacting an experienced Mesa bankruptcy lawyer if you are wishing to stop your wages from being garnished.

Hiring an attorney can help make the process of stopping a garnishment run much more smoothly. Your Mesa garnishment attorney will notify both your payroll department and the creditor who is garnishing your wages regarding you declaring bankruptcy. The automatic stay of the bankruptcy starts as soon as you file and stops the wage garnishment.

It is also important to realize that there are many signs that a garnishment is pending. Prior to a garnishment being put in place; you will receive: First, a law suit Summons. Next, you will get a Notice of Default Judgment, and then finally, a Writ of Garnishment. Filing your bankruptcy proactively upon the receipt of the Summons can make sure that the garnishment never starts.

The experienced attorneys at Mesa Bankruptcy Lawyers can provide you with a clear deadline and target date to file to ensure your case is filed before a garnishment stops. It is important to call our Mesa bankruptcy attorneys and schedule your free consultation as soon as you are served with any legal paperwork. Our Mesa Bankruptcy Team are experienced in stopping wage garnishments and will work with you to help you keep as much of the monies you have worked so hard to earn.

If the chain files bankruptcy, it will more than likely utilize Chapter 11. Chapter 11 can be used by individuals and by businesses, usually those with significant assets and debts that will be particularly complicated to reorganize. Chuck E. Cheese specified that it would be a Chapter 11 filing if the company does end up filing bankruptcy.

If the chain files bankruptcy, it will more than likely utilize Chapter 11. Chapter 11 can be used by individuals and by businesses, usually those with significant assets and debts that will be particularly complicated to reorganize. Chuck E. Cheese specified that it would be a Chapter 11 filing if the company does end up filing bankruptcy. Bankruptcy is a very helpful solution for challenging financial problems. For instance, several individuals have a big charge card debts that become very tough to be worthwhile. These individuals may simply have to create a fresh break with a painful fiscal past and start things over fresh.

Bankruptcy is a very helpful solution for challenging financial problems. For instance, several individuals have a big charge card debts that become very tough to be worthwhile. These individuals may simply have to create a fresh break with a painful fiscal past and start things over fresh.

Declaring bankruptcy stops wage garnishments from creditors where they are in the process. However, you won’t necessarily get any of the money back that has already been taken from you through the garnishment. The idea is to stop a garnishment before your creditors take action against you. That is the best way to assure that you won’t lose any of your hard-earned money in a garnishment.

Declaring bankruptcy stops wage garnishments from creditors where they are in the process. However, you won’t necessarily get any of the money back that has already been taken from you through the garnishment. The idea is to stop a garnishment before your creditors take action against you. That is the best way to assure that you won’t lose any of your hard-earned money in a garnishment.